If you have a “For Sale” sign outside your property right now, you might be noticing a distinct lack of phone calls. You are not alone. A staggering three out of five UK homes listed for sale since January are still sitting unsold, according to Zoopla’s June 2026 House Price Index. If your property is one of them, you already know the intense frustration of watching weeks tick by with zero progress.

Between sudden changes to utility expenses, shifting inflation forecasts, and typical summer holiday distractions, traditional buyers are simply sitting on their hands. Securing a buyer on the open market now takes an average of over 66 days, and that is before the gruelling, multi-month conveyancing process even begins.

Knowing how to sell a house that isn’t selling in a sluggish summer market, without simply slashing your price and hoping for the best, requires understanding what is actually causing the stagnation, not just reacting to it. Buyer demand is down 15% year-on-year. Sales agreed are running 7% behind last year. And the pool of active buyers has shrunk considerably since April, when mortgage rates spiked to nearly 5%. The good news is that homes are still selling. Just not all of them and certainly not by accident.

Contents

- 1 Why Is the Summer Market So Difficult Right Now?

- 2 How To Sell A House That Isn’t Selling Without Dropping Your Price

- 3 What Actually Works on the Open Market

- 4 The Flat Seller’s Problem Is Different, and Harder

- 5 How To Sell A House When You Cannot Afford to Wait

- 6 What the Regional Picture Means for Your Sale

- 7 Taking Control of Your Sale

- 8 FAQs

Why Is the Summer Market So Difficult Right Now?

Imagine a buyer who has been watching the market since February. They have a mortgage in principle, they have done several viewings, but they haven’t quite committed. Then April arrives. Mortgage rates jump from under 4% to almost 5% practically overnight. That adds around £125 a month to the cost of a typical UK mortgage, or £244 a month if they are buying in London. Suddenly, they are not in such a hurry. They will wait and see.

That wait-and-see attitude is now the defining feature of summer 2026, creating a scenario where thousands of homeowners find themselves asking: “Why is my house not selling?”

Several major economic and seasonal factors are converging at once:

1. Mortgage Rate Volatility

Rates peaked in April at close to 5%, up from under 4% at the start of the year, before starting to ease. They now sit around 5.07% on a two-year fix, according to Rightmove’s daily tracker. That is enough improvement to bring some buyers back, but not enough to restore the confidence the market had in January. Buyers are highly sensitive to these small fluctuations, choosing to pause their searches at the slightest hint of an upward trend.

2. The July Energy Price Hike Strain

Compounding the pressure on buyer affordability is the recent 13.5% energy price cap hike that hit UK households on July 1st. While utility bills might seem secondary to a mortgage, traditional buyers are looking at their total monthly outgoings with microscopic scrutiny. This sudden jump in expected running costs has made household budgets tighter, causing a noticeable wave of cold feet and mortgage application pull-backs right at the final hurdle.

3. Record Supply of Houses

There are 13% more homes on the market than at this time last year, according to Zoopla. Buyers have more choice than at any point in eight years. When a buyer has 20 comparable properties to consider instead of five, they take far longer to commit, and they negotiate significantly harder when they finally do make an offer.

4. Seasonal Summer Distractions

Rightmove’s June 2026 data recorded the largest June asking price drop in 14 years, a 0.6% fall taking the average to £376,191. The portal itself pointed to buyers being heavily distracted by summer holidays, major sporting events and early summer heatwaves. These are seasonal factors that are predictable, but they compound the underlying economic drag.

None of this means the market is broken. Well-priced homes are still finding buyers at roughly the same pace as last year.

How To Sell A House That Isn’t Selling Without Dropping Your Price

The standard with an estate agent is to list at the top of the range, wait for viewings, then reduce the price if nothing comes in. This approach is poorly suited to this particular market. If you are stuck in this loop, it is time to look at why the old ways are letting you down.

Zoopla’s own research shows that properties requiring a price reduction took 2.4 times longer to sell than those priced accurately from day one. A reduction does not reset the marketing clock. Instead, it reinforces to savvy buyers that the property has been sitting stale, which raises questions about what might be wrong with it. This leads buyers to either negotiate even harder or move on to fresher listings. Simply reducing your price on portals is not the same as becoming genuinely competitive.

The other traditional failure is treating all buyers as equivalent. A buyer who needs to sell their own home first, secure a high-interest mortgage at current rates and navigate a conveyancing process that takes on average 12 to 16 weeks is carrying an immense amount of risk. In a market where nearly one in four sales still falls through before completion, who your buyer is matters just as much as what they offer. A fractured property chain can instantly set your moving plans back by six months.

What Actually Works on the Open Market

If you choose to stick with the traditional market route, you must abandon passive tactics. To uncover how to sell a house that isn’t selling, you need to execute a precise strategy that addresses modern buyer anxieties:

- Get the pricing right at the outset, not later: Not cheaper, accurate. There is a massive difference. Accurate means based on what comparable properties have actually sold for in your immediate neighbourhood over the last 60 to 90 days, not what they were listed at and certainly not what sold in a completely different interest rate environment. HM Land Registry sold price data is publicly available and gives you the real numbers rather than an estate agent’s optimistic estimate designed to win your instruction.

- Target proceedable buyers exclusively: The buyers in this market are smaller in number but higher in intent, as Zoopla’s index confirms. A committed buyer who has already sold their property and is currently renting, or a first-time buyer with a fully certified mortgage agreement in principle, is worth far more to you than a higher offer from someone who still has a complicated chain to sort out. Instruct your agent to rigorously vet every single buyer’s financial position before viewing slots are allocated.

- Get your legal paperwork in order before listing: Most sellers wait until an offer is formally accepted before instructing a solicitor. This classic mistake adds two to three weeks of pure delay at the start of the legal process. By instructing early, preparing your TA6 and TA10 property information forms, gathering title documents and resolving any outstanding building regulations or planning certificate issues, you compress the post-offer period dramatically. Sellers who prepare thoroughly can cut the total sale timeline by six to eight weeks, keeping momentum alive.

- Audit your online listing with an open mind: In a market where buyers have 13% more choices, your online presentation determines whether a buyer books a physical viewing or swipes past. Professional photography is non-negotiable. If your listing has been live since January with the same winter photos it launched with, it signals to everyone that it is a “problem” property. Refresh it entirely with bright summer photography, update the text layout and consider whether a complete re-listing gives you a cleaner start.

- Advertise your completion flexibility: One of the most underused tools available to sellers right now is flexibility on timing. Buyers in complex situations, such as those relocating for work or coordinating school terms, will often choose a property where the seller can accommodate their specific dates over a slightly cheaper property where the seller is rigid.

The Flat Seller’s Problem Is Different, and Harder

It is worth separating the flat market, because the current data tells a distinctly different and tougher story. Over two-thirds of one and two-bedroom flats listed across the UK remain unsold. This is not primarily a pricing issue; it is a structural buyer-type problem.

Flats, particularly in London and the South East, are heavily dependent on first-time buyers. Unfortunately, first-time buyers are the demographic most acutely affected by elevated mortgage rates and the long-term impact of changes to the stamp duty threshold. In London, four in five first-time buyers now face stamp duty charges of around 3% of the purchase price, compared with under 1% for first-time buyers in the majority of northern England.

This upfront tax cost, layered directly on top of higher monthly mortgage payments and the rising cost of living, has sharply contracted the traditional buyer pool for southern flats. If you are selling a flat in this environment, standard house-selling tips will not cut it. Options worth considering include targeting professional landlords or looking for a fast way to sell an unsold property directly to an institutional cash buyer who can bypass the mortgage application gridlock entirely.

How To Sell A House When You Cannot Afford to Wait

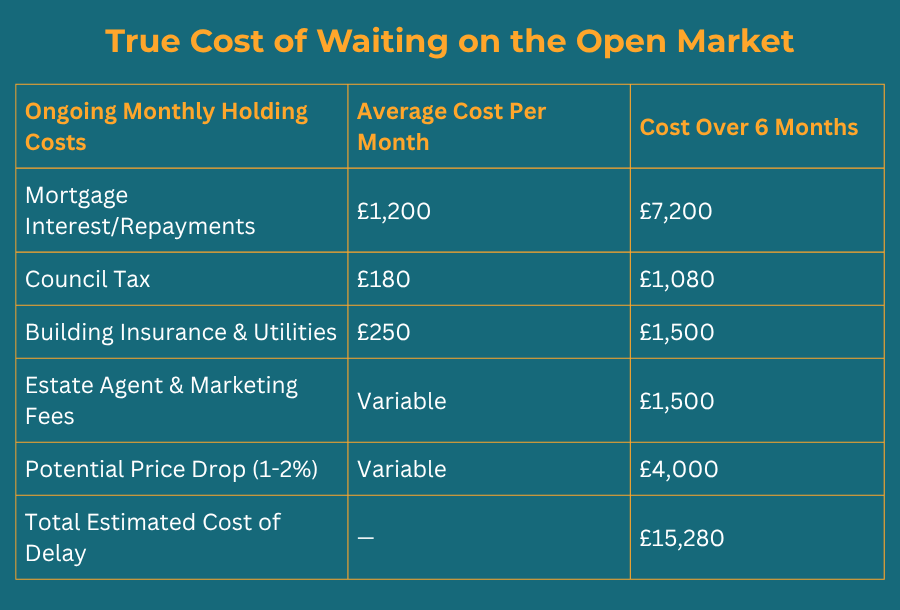

The average time from initial listing to legal completion in the UK currently hovers around 185 days, which is just over six months. For sellers who cannot operate on that extended timetable, whether due to a pending job relocation, a pressing probate estate management situation, financial strain, or simply because they have already suffered a heartbreaking sale fall-through, sitting around waiting for the open market to recover is a high-risk gamble.

This is where understanding the financial trade-offs of a direct cash buying service becomes highly relevant. A professional cash-purchasing route shortens the timeline from six months to as little as 7 to 28 days. The compromise for this extreme speed and absolute certainty is a below-market-value offer. Private cash buyers typically secure properties at around 9.3% below mortgage buyers on equivalent homes, according to MPowered Mortgages’ data. Professional property buying companies, who buy directly and guarantee completion, typically offer between 73% and 85% of market value.

To determine if this route makes sense for you, it is essential to calculate the true ongoing cost of waiting on the open market.

When you factor in these persistent monthly holding costs alongside the psychological strain of multiple failed viewings, the net financial difference between a traditional sale and a guaranteed cash offer often shrinks significantly.

Furthermore, cash transactions fail to complete at a rate of only 4%, compared to a massive 30% failure rate for traditional estate agent sales subject to chains and mortgage approvals. In a volatile summer market, certainty carries a distinct financial premium.

If you do choose to explore the cash buyer route, always protect yourself by verifying credentials. Ensure that any company you engage with holds active membership in the National Association of Property Buyers (NAPB) and is fully registered with The Property Ombudsman (TPO). Legitimate, reputable operators will always display these accreditations clearly.

What the Regional Picture Means for Your Sale

It is vital to recognise that the property market is not a monolith. The latest data reveals a stark geographical divide across the UK, meaning your location dictates your strategy.

In the North East, prices are growing at 3.2% annually, and homes are finding buyers at a healthy pace. Scotland remains the fastest-moving market in the UK, requiring an average of just 31 days to secure a buyer, according to recent data. Cities like Liverpool, Burnley and Rochdale are absorbing fresh housing stock quickly because lower average purchase prices keep properties within reach of buyers despite current interest rates. Sellers in these regions are interacting with a completely different market compared to those down south.

Conversely, London and the South East tell a far more cautious story. In multiple outer London boroughs, homes are taking 50% to 65% longer to find a buyer than they did just twelve months ago. For instance, areas like Harrow are averaging 54 days to find a buyer compared to 33 days last year. Coastal hotspots in southern England, including Bournemouth, Brighton and Truro, currently hold some of the highest concentrations of unsold, stagnant stock in the country.

If your property is located in a northern hotspot, your stagnation may simply be an issue of presentation or minor overpricing. If you are trying to sell a home or a flat in southern England, you are fighting a broader macroeconomic trend and alternative selling methods deserve serious consideration.

Taking Control of Your Sale

Three in five UK homes listed since January remaining unsold is a wake-up call for the industry. This statistic reflects a clear convergence of elevated mortgage rates, a historic surge in property supply, political hesitancy ahead of upcoming fiscal budgets and a seasonal summer slowdown. Knowing how to sell a house that isn’t selling means actively working with these current conditions rather than pretending they don’t exist.

Price your home accurately from day one based on hard sold data, not agent fluff. Target highly proceedable, chain-free buyers. Complete your legal paperwork before you even launch your listing. Completely refresh stale listings rather than relying on endless 5% price drops that signal distress to buyers. And finally, if your personal circumstances mean you simply cannot afford to wait out the summer stagnation, recognise that a genuine, accredited cash buyer offers a practical trade-off, trading a market discount for total completion certainty and immediate relief from holding costs.

Well-priced, strategically managed homes are finding buyers every day. By adjusting your approach to match the realities of the summer 2026 market, you can ensure your property is one of them.

FAQs

Q1: How long does it typically take to sell a house in summer compared to spring?

Spring is historically the most active selling window in the UK property calendar. Zoopla’s historical data indicates that spring listings tend to attract buyers around 20% faster than summer listings. However, this seasonal gap is not an insurmountable obstacle; a perfectly priced property in July will easily outperform an overpriced property launched in April. The heightened risk in summer 2026 is that the baseline buyer pool was already restricted by mortgage costs, making the seasonal summer slowdown feel much more pronounced.

Q2: My estate agent wants me to reduce my price by 5%. Will that actually work?

It depends entirely on the root cause of the stagnation. If your property was launched at an unrealistic premium compared to actual sold prices of similar homes within a half-mile radius over the last 90 days, a 5% reduction is a necessary correction to bring you into the buyers’ search brackets. However, if your listing has simply gone stale from months of exposure, a price drop on its own rarely works. Portals will show the drop, but buyers will still see a high “days on market” counter. You often need a full marketing relaunch, complete with fresh photography, alongside that price adjustment to reset buyer perception.

Q3: Does the type of mortgage my buyer has affect how likely the sale is to complete?

Yes, dramatically. A buyer who possesses a comprehensive “Mortgage Agreement in Principle” is a far stronger prospect than someone who has merely used an online calculator to check eligibility. The strongest mortgage buyers are those who already have a property-specific mortgage offer issued. Mortgage-related fall-throughs are a primary driver of chain collapses; in recent years, mortgage issues accounted for roughly 33% of all failed sales. You are entirely within your rights to request that your estate agent confirms a buyer’s exact financial status and down-payment chain source before you accept an offer.

Q4: If I take my property off the market and relist it, does that reset the days-on-market counter?

On major UK property portals like Rightmove and Zoopla, completely removing a listing for a specified period (typically 14 to 28 days depending on portal terms) and relisting it will reset the public “Added on” date. This can temporarily remove the stigma of a stale listing. However, you must be aware that professional buyer’s agents and data-savvy buyers use browser extensions and Land Registry search tools that expose the full, historic marketing timeline of a property. Relisting must be accompanied by actual changes, like a revised price and brand-new imagery, to be genuinely effective.

Q5: Is autumn likely to be a better time to sell than right now?

Historically, September and October bring a reliable second wave of activity as buyers return from summer holidays and look to complete moves before Christmas. Furthermore, Zoopla forecasts that year-on-year sales comparison metrics should look more favourable in the latter half of 2026 because the final months of 2025 were exceptionally subdued ahead of the previous Autumn Budget. While autumn should bring a slight bump in active buyer numbers, conditions will remain highly dependent on where base interest rates sit. If you have the financial flexibility to pause your sale, refresh your property and relaunch in mid-September with an accurate price, you may find an easier audience than during the July lull.

Related articles