Higher rates and steep living costs have pushed more households into mortgage arrears. UK Finance counts 90,140 homeowner loans and 11,830 buy-to-let loans at least 2.5 per cent behind on payments in the first quarter of 2025. Court filings for possession jumped 34 per cent year-on-year, reaching more than 5,000 claims in three months. While the overall share of loans in trouble is still small at about one per cent, the Bank of England warns that even a modest rise can strain the most vulnerable owners.

Contents

Understanding Mortgage Arrears

Mortgage arrears begin as soon as a borrower misses a full scheduled payment. Lenders label the case “in arrears” once the unpaid sum equals 2.5 per cent or more of the outstanding balance. Letters arrive first; interest and fees follow. If payments stay unpaid, the lender may file a claim in the county court. The law sets a minimum four-week gap between the claim and the first hearing, but judges can move faster.

Why Arrears Are Rising

- Rate resets: Owners who fixed at 2 per cent in 2020 now face rates near 5 per cent, adding £150 a month to the average £250,000 loan.

- Living-cost pressure: Energy, food and council-tax bills still sit well above 2020 levels, squeezing spare income.

- Landlord rules: Buy-to-let owners must plan for an EPC-C upgrade and a higher stamp-duty surcharge, making some choose to sell or risk deeper mortgage arrears.

The Human Cost of Falling Behind

A mark of mortgage arrears sits on a credit file for six years, raising future borrowing costs. Court fees, legal costs and daily penalty interest widen the gap every month. Citizens Advice noted a sharp rise in calls from owners worried about repossession letters in 2025. As mental strain grows, the timeline tightens: the average path from claim to eviction now runs at about forty weeks, shorter than last year, giving families less time to recover.

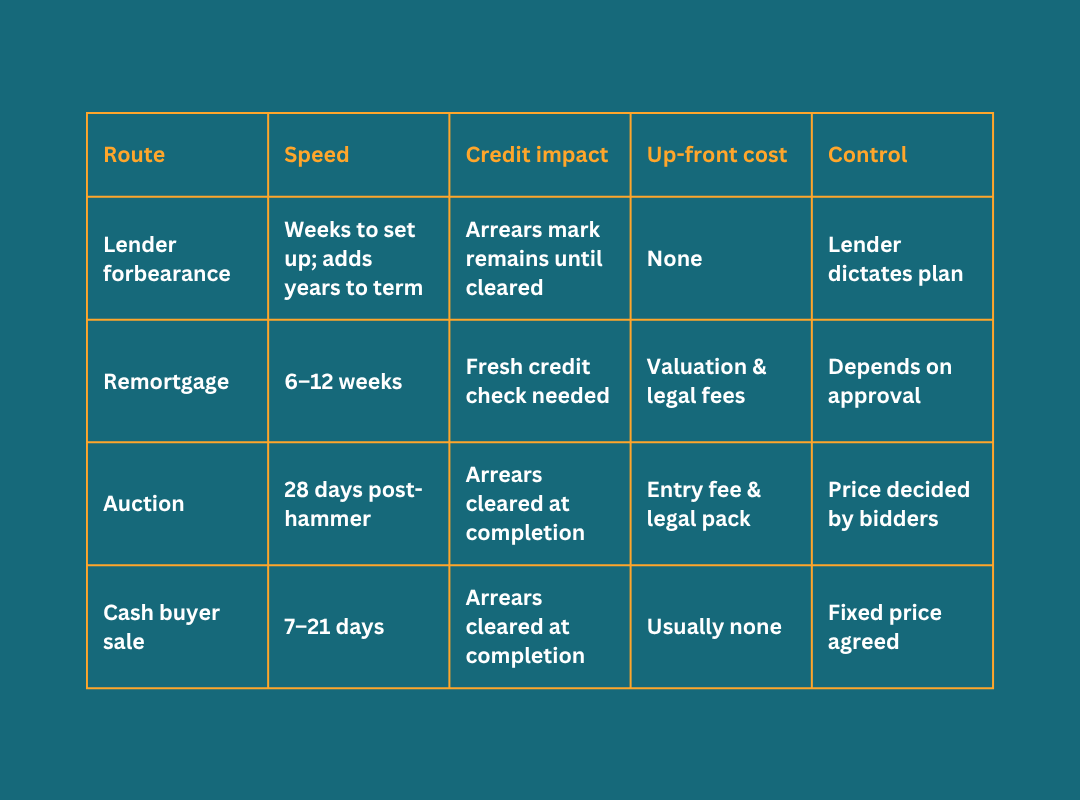

How a Cash-Buyer Sale Breaks the Cycle

What Cash-Buyer Companies Do

Cash-buyer firms use their own funds. They skip mortgage checks and surveys, so they can exchange and complete in days, not months. Many cover the seller’s legal fees and handle all paperwork. Because the buyer pays the lender directly on completion, the arrears stop accruing interest the moment the sale closes.

The Sale Process Step by Step

- Work out the full debt. Ask the lender for an up-to-date redemption figure that includes the arrears, fees, and any early repayment charge. Staying transparent helps later court hearings if the timing slips.

- Get two or more firm offers. Reputable cash-buyer companies will show proof of funds and never demand an up-front fee. The Financial Conduct Authority warns sellers to avoid firms that hide charges.

- Notify the lender. Let the arrears team know a rapid sale is in progress. Judges look kindly on borrowers who stay in contact.

- Exchange contracts quickly. Deals are often exchanged within seven days and completed soon after, clearing the debt before the lender seeks a final possession order.

Auctions as an Alternative

Auction rooms have grown busier, moving more than 28,000 lots in 2024, a jump of almost 11 per cent on the previous year. Auctions offer legally binding sales and 28-day completions, giving owners with mortgage arrears another quick-exit route. Guide prices can be low, so setting a realistic reserve is vital.

Comparing Options

Lender concessions, switching to interest-only or extending the term, can help some, but they lengthen the debt and keep the mortgage arrears flag until fully paid. A fast sale gives a clean break and protects the credit file from the harsher “repossession” note.

Looking Ahead

The Bank of England still pegs headline arrears at about one per cent of all loans, yet it forecasts a steady climb through 2025 as 1.5 million fixed-rate deals reset. Ministry of Justice numbers show that court claims are already back at pre-pandemic levels, and eviction timelines are getting shorter. On the supply side, cash-buyer firms report rising enquiry volumes as owners seek a faster exit to stem mortgage arrears.

Key Takeaways

- Mortgage arrears affect more than 100,000 UK loans today and are climbing again in 2025.

- Court claims for possession rose by a third in one year, tightening the window to act.

- Cash-buyer sales clear mortgage arrears fast, often settling the full debt within two weeks.

- Auctions give another quick-sale path but require clear reserves and entry fees.

- Staying in contact with the lender and seeking advice early gives owners the best chance to avoid repossession.

FAQs

Q1. Is selling with mortgage arrears allowed? Yes. As long as the sale price covers the outstanding balance and costs, the lender must release the charge.

Q2. Do I need lender consent before marketing? No formal consent is required, but telling the lender about the plan shows good faith and may pause further action.

Q3. How much less will a cash buyer offer? Recent studies put the average discount at about 9-20 per cent, reflecting the risk and the speed of completion.

Q4. Will auction buyers pay more? They might, but hammer prices can also fall below reserve. Factor in entry fees and timing risk before choosing this route.

Q5. Does a fast sale erase all mortgage arrears? Yes. On completion day, the buyer’s solicitor sends the full redemption figure to the lender, settling principal, arrears, interest and fees in one transfer.

Related articles

Sell a Hard to Sell Flat in 6 steps

Selling Problem Properties: Why Cash Buyers Are the Solution for Difficult Homes