When facing the reality of divorce, one of the biggest concerns for separating couples is what happens to the marital home. The process of selling after a divorce can be daunting, intricate and emotionally challenging. It’s critical to understand the practical and legal steps involved, as the decisions made will affect the financial stability and future housing arrangements for both parties.

Contents

- 1 Who decides what happens to the home?

- 2 Can an ex force a sale?

- 3 Joint mortgage: protect your credit and speak to the lender early

- 4 Tax points that matter (CGT and timing)

- 5 The three clean choices for the property

- 6 How to sell well on the open market (and keep disputes low)

- 7 Why many couples also line up a cash buyer

- 8 Key takeaways

Who decides what happens to the home?

You and your ex can agree on a plan and record it in a consent order so the court can make it binding. If you cannot agree, a judge decides as part of the financial settlement. Outcomes include: one person buys the other out, a sale now with proceeds split, or a deferred sale (often called a Mesher order) so children can stay until a trigger date. Selling after a divorce often features in these outcomes because a sale can give both sides a clean start.

Mesher orders postpone a sale until a set event (for example, the youngest child reaching 18). They are common when one party cannot take on the mortgage alone, but the court wants stability for the children. If you are discussing a delay, ask a solicitor to explain the triggers, maintenance and who pays what during the deferral.

Can an ex force a sale?

If the home is in joint names, neither person can sell without the other’s agreement unless the court orders it. Where talks fail, the court weighs factors such as needs, children’s housing, mortgage capacity and fairness before ordering a sale, buy-out, or deferral.

Joint mortgage: protect your credit and speak to the lender early

If both names are on the mortgage, both remain liable until the loan is redeemed or transferred, even if one person moves out. Missed payments harm both credit files and can lead to arrears. Tell the lender you are separating; some lenders will agree to short-term forbearance or product changes while you sort the sale or transfer. Keep payments up to date while selling after a divorce so you preserve options and value.

Tax points that matter (CGT and timing)

Transfers between spouses or civil partners on separation benefit from no-gain, no-loss CGT treatment for a defined window under rules updated in recent Finance Acts. That rule can help you move assets between you without triggering a tax bill, especially when you are restructuring who owns the home before or during the sale process. Always check current thresholds and reliefs, including Private Residence Relief, if the property has been your main home. Get bespoke advice if the home has been let or if one of you moved out some time ago.

The three clean choices for the property

1) Buy-out (one stays, one leaves)

You agree on a price, refinance the mortgage if needed and transfer the title. You will still need a consent order to lock the deal into the settlement. This route suits couples who want stability for children, and where one person can afford the loan alone.

2) Sell now and split the proceeds

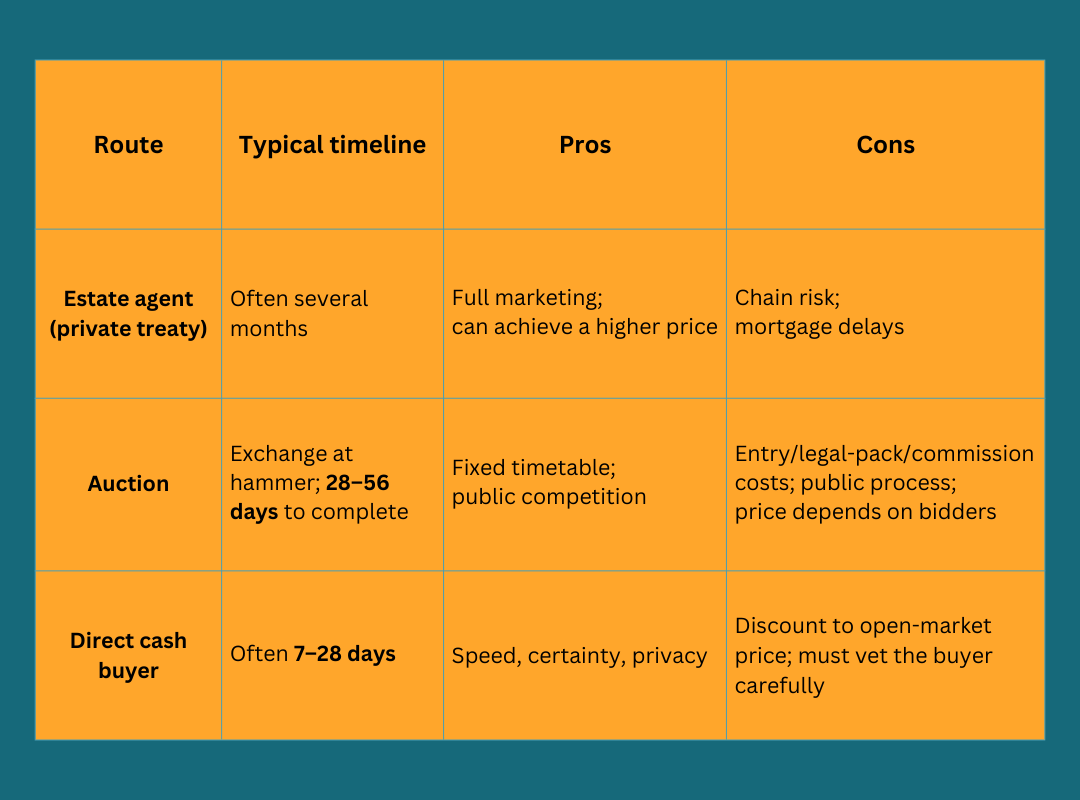

You agree to market the home and divide the net equity per the settlement. This gives both parties cash for fresh housing. Selling after a divorce on the open market can fetch the highest headline price, but timelines are long, and chain risk is real.

3) Deferred sale (Mesher)

You postpone the sale to a trigger date. This protects children’s housing but delays your clean break and can leave two people tied to one mortgage. Balance stability with the cost and admin of staying tied to your ex.

How to sell well on the open market (and keep disputes low)

- Get three valuations and agree on a listing price in writing.

- Assemble documents early: ID and AML, title, EPC, guarantees, consents and a simple list of fixtures and fittings.

- Pick one agent and one conveyancer each to keep lines short.

- Agree on rules on price changes and who pays for minor repairs to avoid fights mid-sale.

- Use mediation to settle disagreements about timing or price before they halt progress.

Why many couples also line up a cash buyer

Open-market chains can take months and collapse late. A cash buyer removes the lender, shortens the chain and gives you a fixed date to plan moves, school terms, or debt clearance. Consumer guidance notes that cash sales are fast and lower risk because there is no mortgage approval, though offers are often at a discount to full market value. The trade-off is speed and certainty vs. a possibly higher – but fragile – open-market price.

Verified benefits of selling to a cash buyer

- Speed: Many professional cash buyers aim to complete in 7–28 days, compared with several months for a standard chain. Good for couples who need funds to rehouse quickly.

- Certainty: No mortgage, no lender valuation, fewer conditions. This helps avoid fall-throughs that are common in long chains.

- Fewer moving parts: You deal with one counterparty; both solicitors focus on title and transfer.

- Privacy and control: No public listing if you sell off-market, which can lower stress in selling after a divorce.

But take care—do basic checks

The quick sale sector is largely unregulated. Get independent legal advice, seek multiple offers and insist on proof of funds and written terms. Some firms pay below market value and you must research providers carefully. Use the due diligence tips below to protect your position.

Open market vs auction vs cash buyer (at a glance)

Due diligence checklist for cash offers

If you choose a cash route for selling after a divorce, use this quick checklist so both of you feel safe and informed:

- Proof of funds: Recent bank statements or a solicitor’s letter covering the full price and costs.

- No “option to reduce” clauses: Avoid contracts that let the buyer cut the price after surveys without strict limits.

- Who pays legal fees: Many firms cover the seller’s legal bill; confirm in writing.

- Deposit on exchange and fixed completion date: Lock in dates that align with your housing plans and school terms.

- Independent solicitor: Each of you should instruct your own conveyancer, even if the buyer offers a “free” lawyer.

- Get two or three cash offers: Compare net proceeds and completion dates before you decide.

Key takeaways

- Agree first, bind it later: Aim for a consent order to fix who gets what, when and how the home will be dealt with. Use mediation to break deadlocks.

- Protect your credit: Joint mortgage = joint liability until redemption or transfer. Tell the lender early and keep payments current.

- Pick the right route: Open market can maximise price; auction gives a firm timetable; a cash buyer offers speed and certainty with a discount; vet providers carefully.

- Mind tax timing: Understand no-gain, no-loss transfers and how CGT and Private Residence Relief might apply when you are selling after a divorce.