When buying, selling, or remortgaging a property, securing a mortgage is usually a key part of the process. However, some properties are deemed “unmortgageable” by lenders, making financing difficult or impossible. Understanding the reasons behind this classification can help homeowners and buyers make informed decisions.

1. Lack of Essential Facilities

A property without fundamental amenities such as a working kitchen or bathroom is often considered uninhabitable. Lenders are unwilling to finance such properties because they require extensive work before being liveable. Mortgage providers prefer homes that meet basic living standards from day one.

2. Structural Defects

Severe structural issues, such as subsidence, large cracks in walls, or roof damage, can make a property unmortgageable. Lenders avoid properties with major defects due to the high cost of repairs and the risk of further deterioration. Structural surveys often highlight such issues, making it harder for buyers to secure financing.

3. Non-Standard Construction

Homes built using non-standard construction materials, such as timber frames, prefabricated panels, or thatched roofs, may not meet mortgage lender requirements. Lenders prefer properties made of brick and mortar due to their stability and ease of valuation. Non-standard materials can present longevity issues and higher maintenance costs, making lenders wary.

4. Short Lease Terms

For leasehold properties, the length of the remaining lease can impact mortgage eligibility. Properties with leases under 70 years are often seen as a poor investment by lenders. Short leases reduce the property’s value over time and may require expensive lease extensions, which add financial risk for both buyers and lenders.

5. Presence of Invasive Plants

Japanese Knotweed is one of the most common reasons a property becomes unmortgageable. This invasive plant can cause structural damage to buildings and is difficult to remove. If lenders identify Japanese Knotweed near a property, they may refuse to issue a mortgage unless there is a professional treatment plan in place.

6. History of Flooding or Subsidence

If a property has a history of flooding or subsidence, obtaining a mortgage can be difficult. Lenders assess the risk of future damage and potential insurance difficulties. Even if flood prevention measures have been implemented, some lenders may still refuse financing due to concerns over long-term stability and insurability.

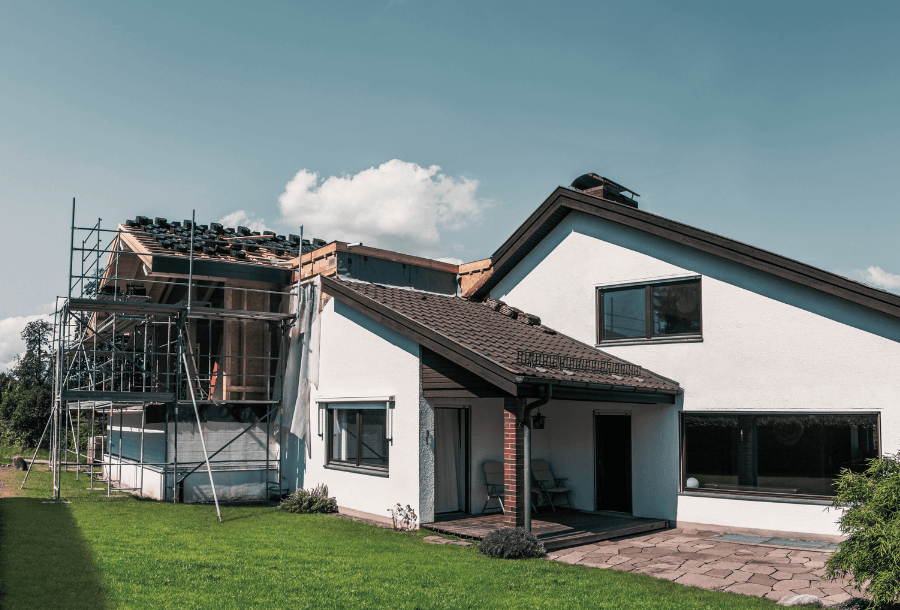

7. Unapproved Alterations or Extensions

Modifications made to a property without the necessary planning permission or building regulation approval can make it unmortgageable. Lenders need assurance that all work meets legal standards and does not compromise the building’s safety or value. If extensions or conversions were completed without the right permissions, lenders are unlikely to approve a mortgage.

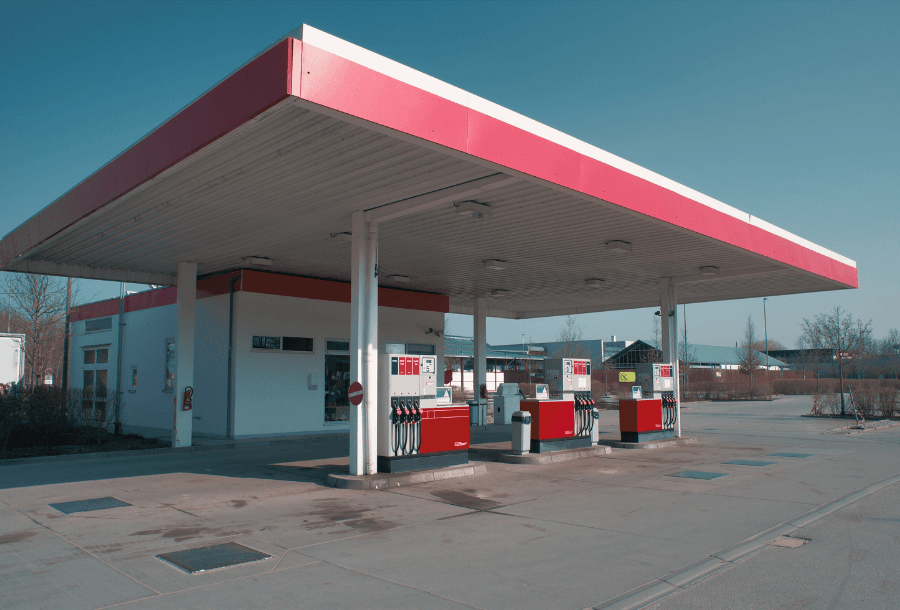

8. Proximity to Commercial or Industrial Sites

Homes located near busy commercial or industrial areas may struggle to secure a mortgage. Lenders assess desirability and marketability when approving loans. Properties close to pubs, restaurants, factories, or petrol stations may be considered less attractive due to noise, pollution and potential future resale difficulties.

9. Low Property Value

Some lenders have a minimum property value requirement, often around £40,000 to £50,000. Properties valued below this threshold may be deemed unmortgageable because the lender sees little return on investment. Low-value properties can also indicate structural or location issues, making them a higher-risk investment for lenders.

10. Environmental Hazards

Properties built on contaminated land or near environmental hazards such as former landfill sites, high-radon areas, or mining sites can struggle to secure mortgage approval. Lenders consider the long-term safety and habitability of a property when assessing mortgage risk. If there are environmental concerns, they may refuse to finance the purchase.

11. Properties with Sitting Tenants

If a property is sold with a sitting tenant under a protected tenancy agreement, securing a mortgage can be difficult. Some lenders refuse to finance properties where tenants have long-term rights, as this limits repossession options if the borrower defaults on repayments. The inability to regain vacant possession reduces the property’s appeal for mortgage providers.

12. Properties Above or Near Commercial Premises

Flats located above shops, takeaways, or bars can face mortgage restrictions. Lenders worry about resale potential, noise levels and the impact of business operations on the property. Some lenders will still offer mortgages on such properties, but the options may be limited, requiring larger deposits or specialist lenders.

13. Title Deed Issues

Issues with property title deeds, such as unresolved disputes, missing documentation, or unclear ownership, can make a property unmortgageable. Lenders require a clear and legally binding title to approve a mortgage. If there are discrepancies or outstanding legal complications, mortgage applications may be denied until the issues are resolved.

Shared ownership properties or those with restrictive covenants can be challenging to mortgage. Lenders may be reluctant to approve loans on homes with restrictions on how they can be sold or used. If a property has conditions limiting future modifications or requiring approval from a third party, mortgage options may be limited.

15. Ex-Local Authority Properties

Some ex-council or local authority properties, especially those in high-rise buildings, may be considered unmortgageable. Lenders assess the construction quality and demand for such properties. If a property has limited resale potential due to its past as social housing, obtaining a mortgage can be more difficult.

Key Takeaways

- Properties must meet basic living standards, including having a functional kitchen and bathroom, to be mortgageable.

- Structural soundness and standard construction materials improve mortgage approval chances.

- Environmental and location factors, such as flooding history or proximity to commercial sites, can impact mortgage eligibility.

- Legal and documentation issues, including title deed problems and unapproved modifications, can make a property unmortgageable.

FAQs

Q1: Can I still buy an unmortgageable property? Yes, but you may need to use cash or seek alternative financing such as bridging loans or specialist lenders.

Q2: How do I fix an unmortgageable property? Addressing structural issues, obtaining missing paperwork, extending a short lease, or securing treatment for Japanese Knotweed can help make a property mortgageable.

Q3: Can I get a mortgage on a property with a short lease? Some lenders will consider financing if the lease is extended first, but this process can be expensive.

Q4: How does Japanese Knotweed affect mortgage approval? Lenders often require professional treatment plans and guarantees before considering a mortgage on a property affected by Japanese Knotweed.

Q5: Can I get a mortgage on a non-standard construction property? It may be possible, but lenders offering mortgages on non-standard homes often require larger deposits or higher interest rates.

Relate articles